The June inflation report just came out and the number was 9.1%. A lot higher than was initially anticipated and now you have all the prognosticators in the market and the media coming out and arguing why that is the case. Watch Casey Marx RICP® Discuss The June...

Flip Flop U.S. stocks posted modest weekly gains, reversing the negative trend of the previous week. There was a wide divergence across the major U.S. indexes, with the NASDAQ gaining nearly 5%, the S&P 500 adding 2%, and the Dow rising less than 1%. Yield Curve...

Roaring BackAfter declining for three weeks in a row, the major U.S. stock indexes regained their footing, with the NASDAQ surging more than 7%, the S&P 500 adding more than 6%, and the Dow rising more than 5%. The results marked a near mirror-image reversal from...

The 3.9% sell-off on Monday pushed the S&P 500 into a bear market, as the index’s decline from a record high achieved on January 3, 2022, exceeded 20.0%. The NASDAQ has been in a bear market since March, while the Dow on Friday was just shy of a bear, as it...

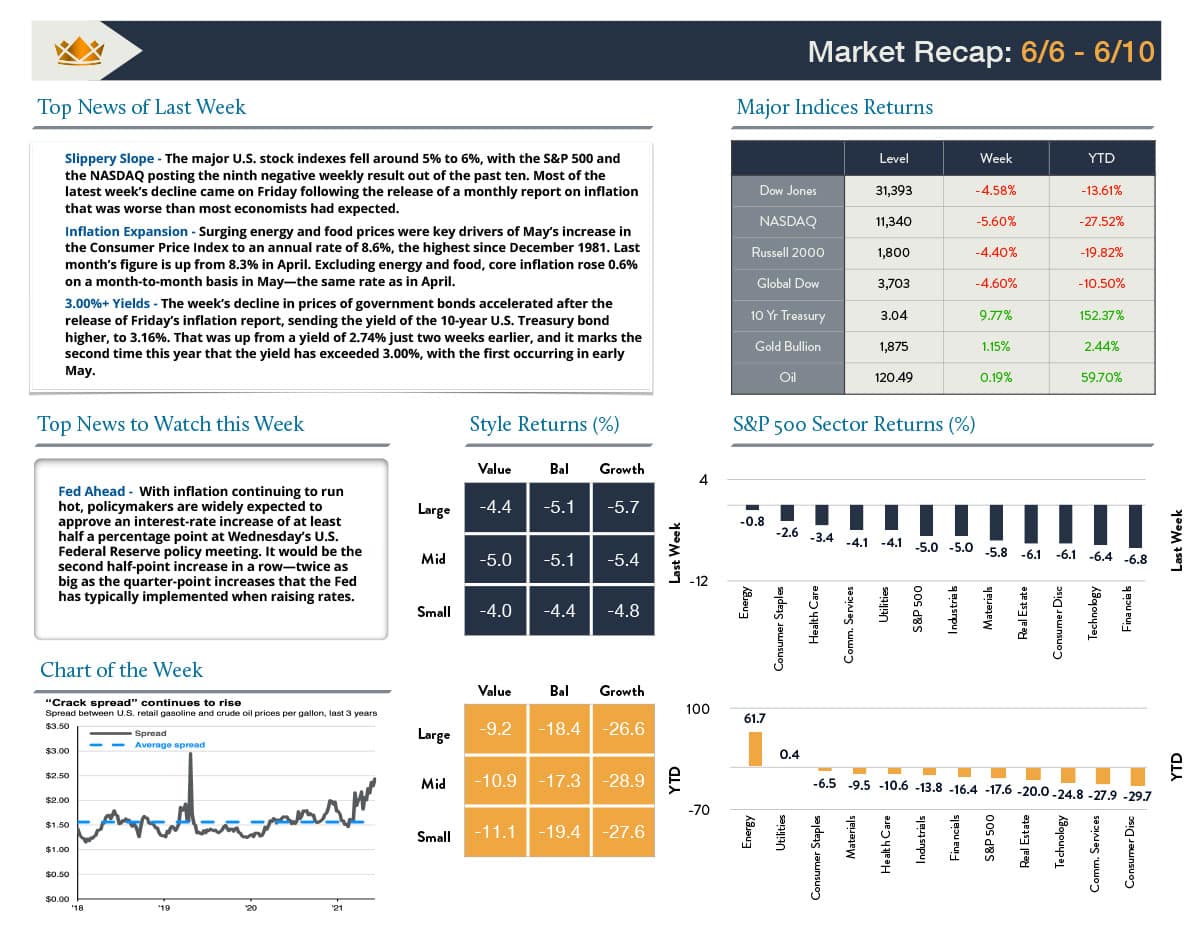

Please enjoy the 6/13/22 Wealth Management Insights edition from Crown Haven Wealth Advisors, Indiana’s #1 independent and fiduciary full-service firm. Slippery Slope – The major U.S. stock indexes fell around 5% to 6%, with the S&P 500 and the NASDAQ...

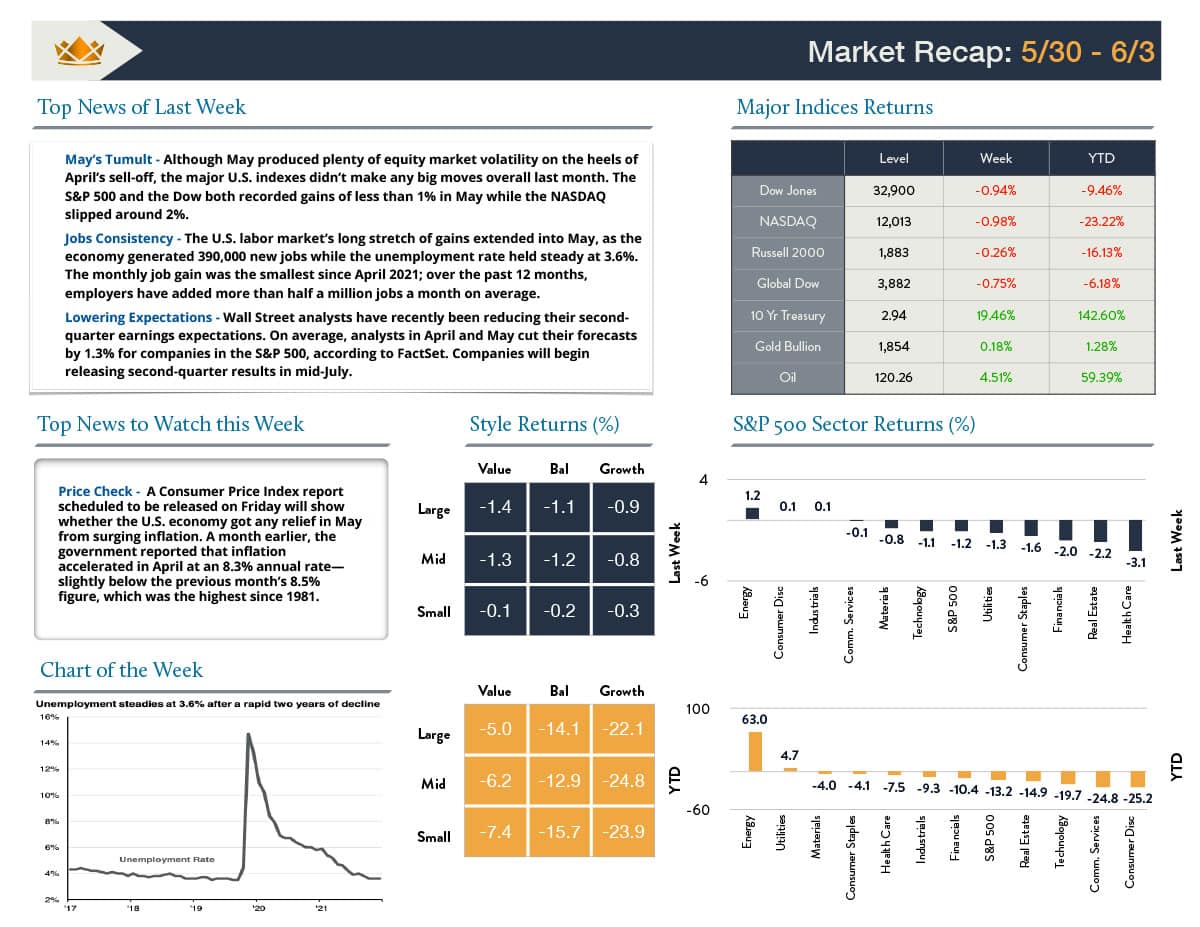

Please enjoy the 6/06/22 Wealth Management Insights edition from Crown Haven Wealth Advisors, Indiana’s #1 independent and fiduciary full-service firm. May’s Tumult – Although May produced plenty of equity market volatility on the heels of April’s...