Casey Marx our founder and CEO of Crown Haven Wealth Advisors. Marx was just interviewed by Samantha Johnson of WTHR about why more Hoosiers are retiring early and how they are pulling it off? n our work with financial planning clients, we have seen the pandemic serve...

Managing the risk of outliving your money has become one of the top questions we hear from pre-retirees. In fact, according to TransamericaCenter.org research1, 42% of workers say they fear outliving their savings and investments. Retirees face greater...

Here are 3 financial planning tips for the second half of 2022. With half the year behind us, now is a great time to consider what the remainder of 2022 may hold. However, with inflation and economic uncertainty causing many of us to delay or cancel vacations, large...

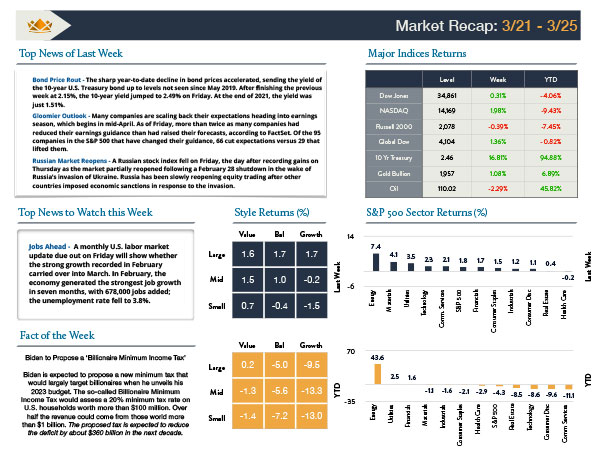

Bond Price Rout- The sharp year-to-date decline in bond prices accelerated, sending the yield of the 10-year U.S. Treasury bond up to levels not seen since May 2019. After finishing the previous week at 2.15%, the 10-year yield jumped to 2.49% on Friday. At the end of...

2022 brings new tax and saving changes that could impact your finances. Updates include standard deductions, retirement-plan contributions, estate, and gift tax changes are the federal government’s effort to the American people feel fewer effects of record-high...

Here is a question about your retirement plan and when your investments lose value. Whether it’s your 401(k), IRA, Roth IRA, Rollover IRA, or other financial accounts. It could be stocks, mutual funds, REITs or other investments. How much better off would you be...