Who We Are

Creating Relationships, Building Trust, Sharing Expertise & Delivering Results – Since 2011

Creating Relationships, Building Trust, Sharing Expertise & Delivering Results – Since 2011

To ensure you spend less time worrying about your money and more time enjoying your life.

To be the last advisor you ever need.

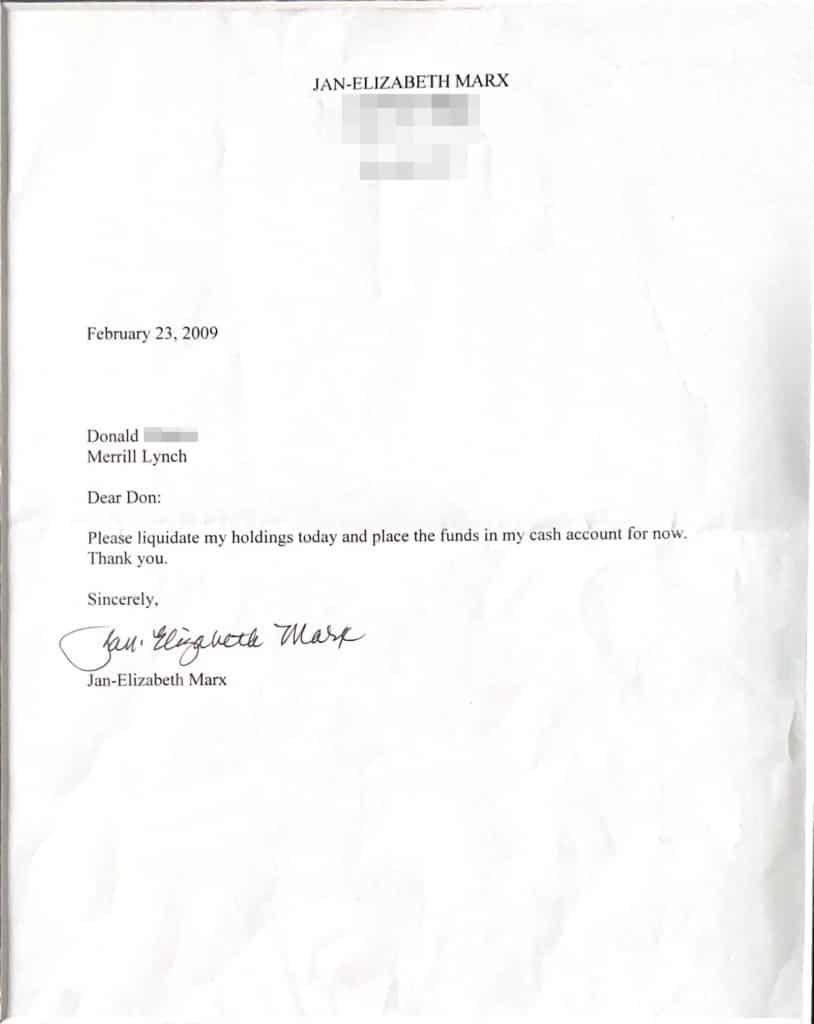

Casey Marx’s Mother’s Original Liquidation Letter

Casey Marx and his Mother

The financial crisis of ‘08/‘09 destroyed millions of family’s life savings, and Casey Marx’s (our founder) family was no exception.

The letter above stated Casey’s mother’s intention to divorce herself from her “advisor” at a “Big 5” broker/dealer and take back control of her financial future.

Casey’s dad had died when he was 15, and as an only child, he watched his mother lose more than half of her life savings within a blink of an eye – while the advisor was supposed to be minding the store.

At the time, Mr. Marx was in college pursuing a degree in medicine.

He didn’t intend on becoming a wealth advisor or retirement planner, but sometimes in life, your passion finds you.

Casey knew he wanted to prevent what happened to his mother from ever happening to her again, but when he began to look at the bigger picture, he realized she needed help with a lot more than just investing.

For instance, upon retirement, his mother was going to need to use her investments to replace her income she enjoyed from employment in a safe and sustainable way.

How would she accomplish this? What about taxes? How could she keep more of her hard-earned dollars to use for herself, now and in the future?

Making decisions about when to take social security and the options with her pension was a whole other conversation, and so was healthcare in retirement – she was terrified of getting sick and going broke.

What about her legacy? She wanted to make sure that her money went to the people she cares about, and her wishes were carried out properly.

When Mr. Marx examined the financial services industry and why it had failed his widowed mother, he was sick to his stomach.

The truth is that unless you are ‘ultra-high net worth’, most firms view it as a waste of time to offer additional guidance for these areas; there simply isn’t enough of a financial incentive to do so.

Meanwhile, if you’re a “normal person” the typical financial advisory firm simply wants to capture your assets and charge you a fee to invest your money (usually in the same thing they invest everyone else in).

The typical advisor’s goal is for your investments to perform on par with the market because so long as this is accomplished, they are in the clear from a regulatory standpoint and you typically won’t leave them.

This means that the end result of your relationship is that you ride the market and pay the advisor a fee whether you win or lose, while the advisor or firm creates more and more revenue by obtaining more accounts like yours, creating more passive residual income for the advisor (or firm).

There is no customization, there is no relationship, and there are no solutions offered for the many real needs you have.

The truth is that much of the financial advice industry is a fundamentally flawed sales system, and it’s sad.

The reason Crown Haven was founded is because we believe EVERYONE deserves great advice, from a team of expert professionals that truly care about your outcome.

That’s also why we created our registered RetireSHIELD® program, which is designed to eliminate threats and take advantage of opportunities in 5 key areas – the critical areas that ensure that you experience a life without financial stress – which allows for you to pursue your own version of happiness; whatever that means to you.

Since 2011, clients with greatly different financial needs and situations have come to Crown Haven looking for customized wealth management strategies to meet their unique needs.

Our experience working with high-net-worth individuals, small-business owners, accredited investors, young professionals, or those planning for, entering, or in retirement, has led to our development of time-tested and experience-based frameworks for building wealth management strategies tailored to the individual goals, needs, and objectives of each client

Crown Haven is located in Carmel, Indiana, and serves clients in Zionsville, Westfield, Fishers, McCordsville, Whitestown, Brownsburg, Noblesville, Cicero, Lawrence, Clermont, Lebanon, Pendleton, Avon, Plainfield, Northfield, and Fortville. We also have clients in the neighborhoods of Meridian Hills, Meridian Kessler, Butler–Tarkington, Spring Mill, Towne Road, and more. Our reputation has spread outside of the Indianapolis area, and we have clients all over the great state of Indiana and across the United States.

Since our inception, Crown Haven has been a fee-based fiduciary advisor for our clients, always using the Fiduciary Standard as the bedrock of our planning philosophy.

A Fiduciary is an advisor that is bound to the Fiduciary Standard – an advisor that must always put their client’s interest first.

Crown Haven approaches this responsibility by operating with the same care and attention that we would use with our own money.

We believe that any great relationship requires trust, and the advisor-client relationship is no exception. This is why one of Crown Haven’s core values is to be entirely transparent with our clients regarding all aspects of their financial plan. If you have any questions about any aspect of our wealth management, please reach out to us – we are happy to help.

An investment adviser’s fiduciary duty under the Advisers Act comprises a duty of care and a duty of loyalty. This fiduciary duty requires an adviser “to adopt the [client’s] goals, objectives, or ends.”

This means the adviser must, at all times, serve the best interest of its client and not subordinate its client’s interest to its own.

In other words, the investment adviser cannot place its own interests ahead of the interests of its client. This combination of care and loyalty obligations has been characterized as requiring the investment adviser to act in the “best interest” of its client at all times.

U.S. Securities & Exchange Commission (SEC) Commission Interpretation Regarding Standard of Conduct for Investment Advisers